(5 min read)

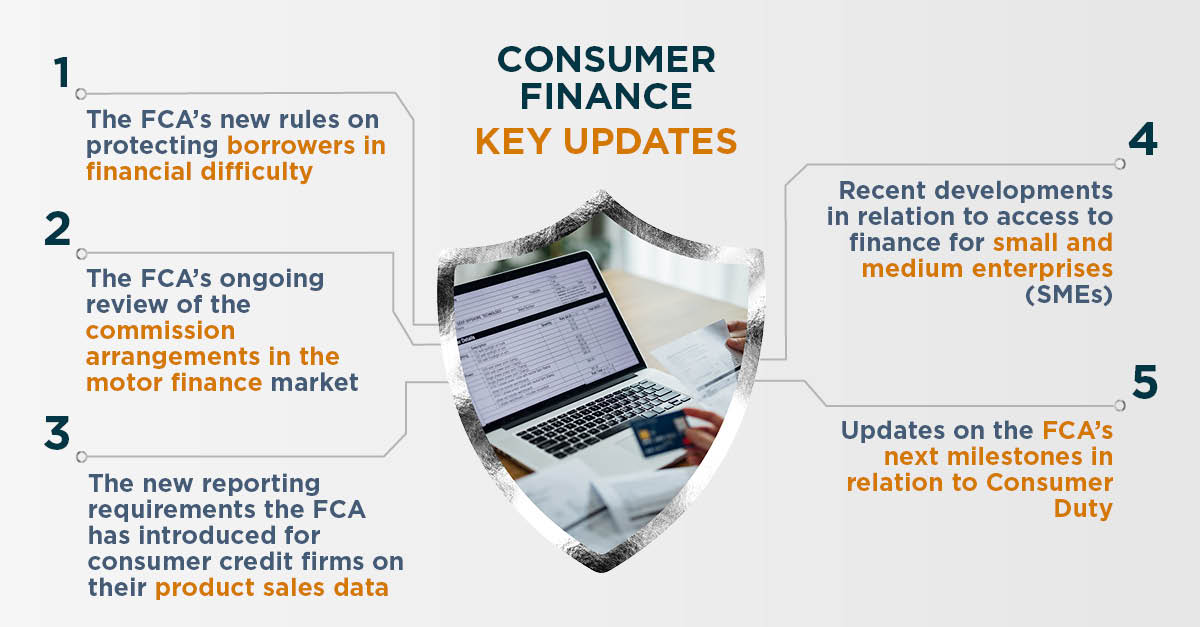

In this edition, we discuss the FCA's new rules for enhanced forbearance options for borrowers in financial difficulty, an ongoing review of motor finance commission arrangements, new reporting requirements for consumer credit firms, and improvements in finance access for SMEs. Additionally, there is an update on the FCA's upcoming milestones related to Consumer Duty. These changes impose strict regulatory deadlines and offer new business opportunities.

FCA policy statement on strengthening protections for borrowers in financial difficulty: Consumer Credit and Mortgages

On 10 April 2024, the Financial Conduct Authority (FCA) published a policy statement (PS24/2): Strengthening protections for borrowers in financial difficulty: Consumer Credit and Mortgages. Through this policy the FCA is making changes to its forbearance rules and guidance – effective from November 2024. The new rules will require mortgage and consumer credit firms to provide enhanced support to their customers who are both in and at risk of financial difficulty. Firms need to consider these requirements very carefully and assess what changes to their current agreements, policies and processes would be required to ensure compliance before the November 2024 deadline.

Read what is required under the new rules

FCA's ongoing motor finance commission review and current status

On 11 January 2024 the FCA announced that it will be undertaking work in relation to the historical use of discretionary commission arrangements (DCAs) in the motor finance market which were banned in 2021. Motor finance firms need to review their existing complaints procedures in relation to DCA complaints and complying with new rules and requirements. Lenders in the motor finance market may also be required to pay significant consumer redress by the FCA later this year, if it finds there has been widespread misconduct and consumers have lost out as a result.

Read here to know further on these requirements

FCA policy statement on new product sales data returns for consumer credit firms

The FCA has introduced new reporting requirements for consumer credit firms. The requirements are now being imposed on wider consumer credit market who were outside the scope of the FCA's Product Sales Data (PSD) reporting rules which were much smaller in scope and were only limited to firms undertaking high-cost short-term credit and home-collected credit. The new rules are creating some very complex thresholds and milestones that relevant firms should consider carefully in determining how these requirements will apply to them. Firms have a significant amount of preparation to undertake to meet the new requirements. This also highlights the FCA's ongoing shift towards becoming a more data-driven regulator.

Click here to know more about these requirements and the strict regulatory deadlines that are being imposed on firms

SME's access to finance - recent developments

The regulation of SME lending continues to be a hot topic with two recent developments. First, the report from the House of Commons Treasury Committee following its long-running inquiry into SME's access to finance; and second as well as the FCA's response to the Federation of Small Businesses' (FSB) 'super-complaint' regarding the current lending practices of banks that demand personal guarantees for business loans. The debate on the extension of the regulatory perimeters for SME lending is live as the review of the Consumer Credit Act 1974 retained provisions gathers pace and the potential for the expansion of the regulatory perimeter for SME lending as part of that review remains a possibility.

Discover more on these developments

Consumer Duty - next steps

As we know the Duty isn’t a "once and done" event. It’s something that needs to shift from one-off implementation activity to become part of the firm's culture and business, running across its whole organisation from Board to front-line delivery, from product design to communications and customer support. In its recent publications, including the findings from its review of consumer duty implementation, the FCA has set some key focus areas and milestones that the firms should be looking at to meet the ongoing expectations under the Duty.

Read more here to see what those focus areas are