Executive Summary

On 12 September 2024, the PRA launched its consultation on its proposed simplified capital regime for small domestic deposit takers (SDDTs) alongside its publication of the second near-final policy statement implementing the Basel 3.1 standards. As well as engaging with the consultation, SDDT-eligible firms now face a choice as to which capital regime is right for their business and future strategic plans.

The PRA proposes a number of simplifications to the calculation of Pillar 1 and Pillar 2A capital requirements, ICAAPs and reporting for SDDT firms. It also proposes to replace the current capital buffers with a Single Capital Buffer, set at no less than 3.5% of RWAs.

Opting into the SDDT regime is optional for SDDT-eligible firms and some firms have already opted into a simplified regime for liquidity and disclosure requirements. Ordinarily, SDDT-eligible firms must be UK owned and focussed firms with total assets that do not exceed £20billion. However, foreign-owned UK subsidiary firms may apply to be treated as SDDT firms at the PRA's discretion if certain criteria are met. SDDT-eligible firms cannot use an internal ratings-based approach and must not carry out markets or trading activities. Our view is that the data-flows from firms around these thresholds will be a focus for the PRA, alongside wider data initiatives.

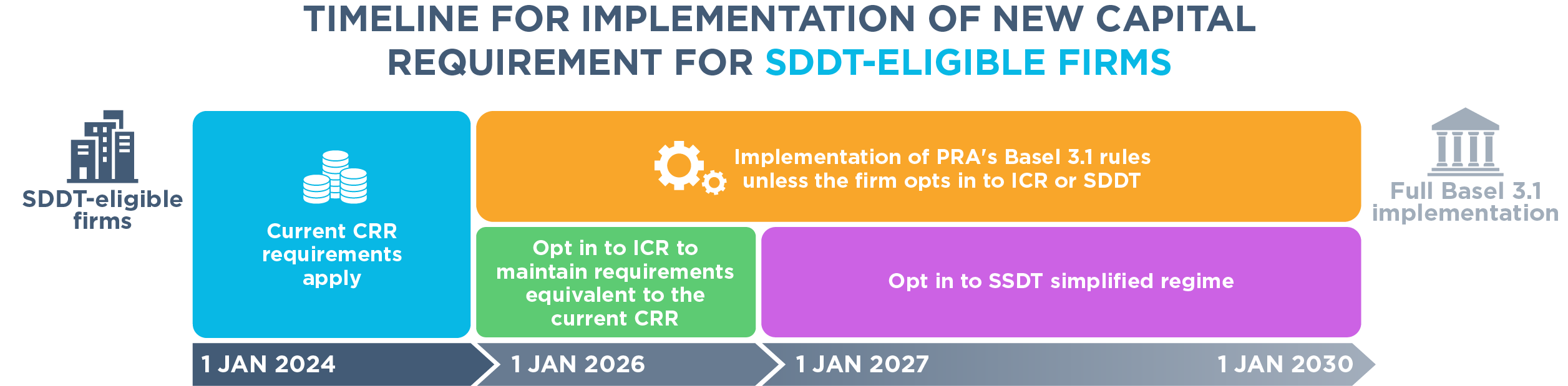

The PRA expects the new simplified capital rules under the SDDT regime to come into effect on 1 January 2027. This is a year later than the expected implementation of the PRA's wider Basel 3.1 package. In the interim, SDDT-eligible firms (including approved foreign-owned subsidiaries) can elect to enter a transitional arrangement called the interim capital regime (ICR). They will then continue to be subject to requirements equivalent to those under the existing Capital Requirements Regulation until the SDDT regime is in force.

SDDT eligible firms will need to carefully consider the impact of the PRA's proposed changes, taking account of their future strategic plans and the costs of implementing the new requirements on the timetable expected by the PRA.

The deadline for responding to the PRA consultation is 12 December 2024.

Under the final package of Basel 3.1 measures, the PRA has responded to industry feedback, and addressed a number of concerns relevant to SDDT-eligible firms, including in relation to SME and infrastructure lending and the valuation of real estate assets. The new standardised approach to credit should be more risk sensitive for all firms. We will discuss the key elements of the PRA's wider Basel 3.1 implementation in a separate publication. This publication focuses specifically on the proposals relating to the SDDT regime.

SDDT framework: the story so far….

On 5 December 2023, the PRA published a policy statement and final rules establishing and implementing the first part of the SDDT framework, also referred to as the "Strong and Simple" framework. Solo firms or firms part of a wider consolidation group which meet the criteria set out below (SDDT firms) can seek permission from the PRA to be subject to simplified liquidity and Pillar 3 disclosure regimes. Eligible firms have been able to opt in since 1 January 2024, from which point the modified disclosure rules applied. The modified liquidity rules have applied from 1 July 2024.

The criteria for the SDDT regime apply on a solo basis for firms without a wider UK consolidation group and on a solo and group basis for firms that are part of a UK consolidation group, where every firm within the group will also need to meet the scope criteria. They are broadly:

- total assets do not exceed £20 billion;

- on average, at least 85% of credit exposures over the last three years are to be in the UK, with a minimum at any time of at least 75%;

- a trading book business less than or equal to the lower of £44 million or 5% of the firm's total assets;

- an average foreign exchange position of not more that 2%, and never more than 3.5%, of its own funds;

- no positions in commodities or commodities derivatives;

- no use of an IRB model for credit risk;

- no clearing, settlement, custody or correspondent banking, or operation of a payment system; and

- the parent undertaking of the firm is in the UK (unless the PRA grants an approval to a foreign-owned subsidiary firm).

SDDT framework: so what's new?

On 12 September 2024, the PRA published a consultation paper setting out the proposed capital regime for SDDT firms. This was published alongside the PRA's second near-final policy statement on the implementation of the Basel 3.1 standards in the UK.

The PRA proposes a simplified version of its capital regime which SDDT-eligible firms can elect to opt into, should they wish. The table below sets out the key areas of difference between the PRA's proposed SDDT regime and the requirements that apply under the PRA's Basel 3.1 implementation.

Click here to view the table

SDDT framework: timing and transitionals

The PRA proposes that firms which have opted into the SDDT regime will be subject to the simplified rules in relation to capital from 1 January 2027. SDDT-eligible firms need only opt into the SDDT regime once, which will allow them to apply both the existing simplified rules on liquidity and disclosure, and the simplified capital rules, when they come into force.

The PRA's implementation of Basel 3.1 is expected to be 1 January 2026, with a transitional process of 4 years to ensure full implementation by 1 January 2030. To avoid SDDT firms needing to implement Basel 3.1, the PRA is creating the ICR for SDDT firms. This would allow SDDT-eligible firms to choose to continue to be subject to requirements equivalent to the existing Capital Requirements Regulation rules, rather than needing to implement the new Basel 3.1 rules, until the introduction of the SDDT capital framework on 1 January 2027. Opting in to the ICR is a separate process from opting into the SDDT. This implementation timeline is set out below.

SDDT framework: is it for you?

SDDT-eligible firms have a choice whether to take advantage of the SDDT regime (and the transitional regime under the ICR), or move to implement the PRA's Basel 3.1 package. A firm can leave the SDDT regime at any time once subject to it, either by choice or because it no longer meets the SDDT criteria.

That decision will be driven by the individual position and future strategic plans of each firm. Some aspects firms will need to consider include:

- Whether the firm's future growth plans may take it outside of the criteria for the SDDT regime, for example a plan to expand outside of the UK or into trading activities;

- the operational costs and resources necessary to build required new systems, set in the context of the firm's future plans and the PRA's implementation timetables for both Basel 3.1 and the SDDT regime;

- the application of the PRA's wider Basel 3.1 package to the firm's business, and the value to the firm of the simplifications available under the SDDT regime; and

- the ability of the firm to leave the SDDT regime at any time once subject to it.